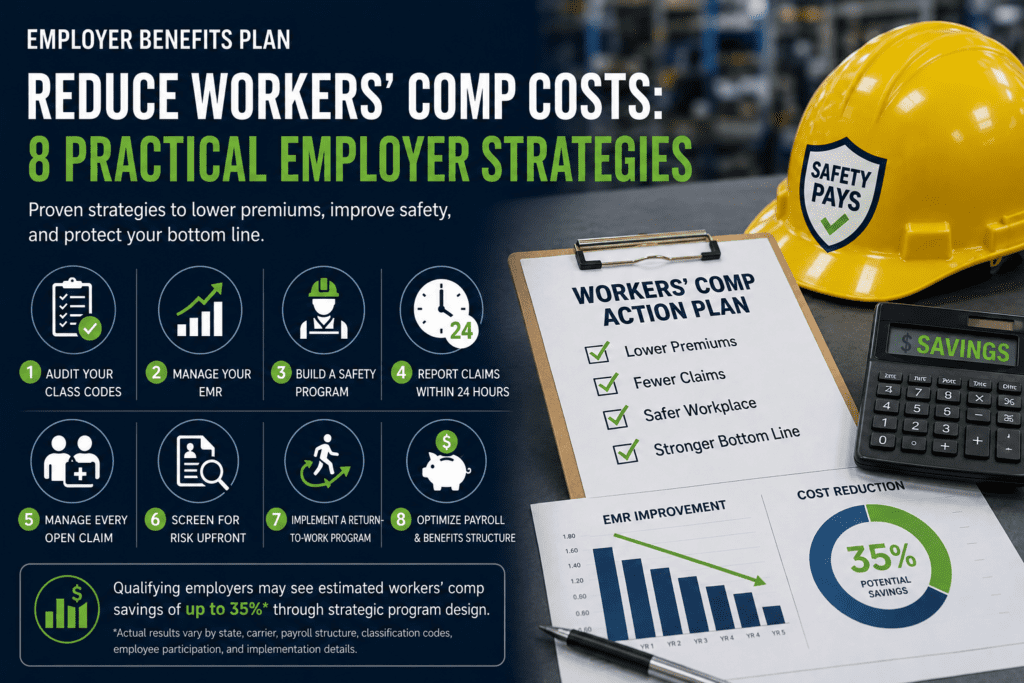

Reduce Workers’ Comp Costs: 8 Proven Employer Strategies

Workers’ compensation premiums are among the most controllable cost lines on your P&L, more so than most employers

realize. Most treat them as a fixed expense, pay the invoice, and move on. That’s a mistake. Premium costs are driven by a

handful of specific levers: classification codes, claims history, payroll structure, and safety performance. Pull the right ones

in the right order and the savings compound year over year.

The strategies below show how to reduce workers’ compensation costs across classification audits, EMR management,

claims protocols, return-to-work programs, pre-employment screening, and a payroll structure approach that most

employers have never encountered. One of the least-discussed tactics involves how payroll and supplemental benefits are

structured together. In some cases, qualifying employers may see estimated workers’ comp savings of up to 35%, based on

program modeling and internal client analysis. Actual results vary by state, carrier, payroll structure, classification codes,

employee participation, and implementation details.

Each strategy below comes with a specific outcome or savings figure attached. Use this as a prioritized action plan, not just

a reading list.

1. Audit your classification codes before doing anything else

Most employers overpay before a single claim is ever filed. Workers’ comp premiums are calculated as payroll divided by 100, multiplied by the class code rate, multiplied by your EMR. Each class code carries a different rate per $100 of payroll, and the spread between codes is significant. A field technician coded as a construction worker instead of a clerical employee can mean substantially higher rates on that portion of payroll, in some cases several times more, depending on state rate tables published by NCCI or your state rating bureau.

Misclassification often goes uncorrected without proactive audits. Pull your current class code assignments from your policy, compare them against NCCI or your state-specific definitions, and flag any employees coded above their actual job

duties. Many carriers will adjust classifications when errors are documented, and back-audits can sometimes recover overpayments from prior policy periods, though carrier obligations vary by state and insurer policy language.

KPI to track: premium per $100 of payroll by department before and after correction.

KPI to track: premium per $100 of payroll by department before and after correction.

2. Understand your EMR and what moves it

Your experience modification rate is a multiplier on every dollar of premium. It compares your actual losses to the expected

losses for your industry. A 1.0 is average. Above 1.0 costs more; below 1.0 earns a discount. The dollar impact is direct: an

employer with a $200,000 base premium at 1.2 EMR pays $240,000. At 0.8 EMR, they pay $160,000. That’s an $80,000

swing with no change in coverage.

EMR is recalculated annually using three years of loss history, so improvements today typically show up in your rate within 12 to 24 months as prior years roll off your experience period. The inputs with the biggest impact are claim frequency (more claims raise it faster than you’d expect), open reserve amounts on active claims, and payroll classification accuracy. Attacking all three simultaneously produces the fastest EMR improvement, and the most durable workers’ comp cost reduction over time.

EMR is recalculated annually using three years of loss history, so improvements today typically show up in your rate within 12 to 24 months as prior years roll off your experience period. The inputs with the biggest impact are claim frequency (more claims raise it faster than you’d expect), open reserve amounts on active claims, and payroll classification accuracy. Attacking all three simultaneously produces the fastest EMR improvement, and the most durable workers’ comp cost reduction over time.

3. Build a safety program that actually reduces workers' compensation costs

Formal safety training programs produce roughly 24% fewer injuries on average, and broader safety investments return $4

to $6 for every $1 spent, according to OSHA training statistics. One widely referenced figure from a NIOSH-funded analysis

puts the ROI at $4.41 saved per $1 invested (NIOSH-funded analysis). These aren’t theoretical numbers; they reflect real

reductions in claim frequency, which is the fastest driver of EMR improvement.

The training format matters. Hands-on, behavioral training with real-world scenarios outperforms passive lecture-only

formats. Annual or biannual refreshers sustain the gains over time by reinforcing safe behaviors before they erode. Industry

benchmarking data indicates organizations with comprehensive safety programs report 20% or greater reductions in injury and illness rates, making loss control and workplace safety one of the highest-leverage areas for sustained premium

reduction.

KPIs to track: injury rate per 100 employees, lost-time claim frequency, year-over-year EMR movement.

4. Report every claim within 24 hours

Delayed reporting is a silent premium killer, and the cost penalties are measurable. Claims reported within 24 hours cost 30

to 50% less than claims reported after a week, based on insurance industry claims analysis. A two-week delay increases

average claim cost by 18%. A five-week delay pushes that increase to 45%. Back injuries specifically run approximately 35%

more expensive when not reported within the first seven days.

The litigation risk compounds quickly: 47% of claims reported after four weeks become litigated, adding another 30% to

average costs. Designate a single point of contact for all incidents, set a same-day or next-day reporting requirement in

writing, and train every supervisor on the protocol. This one change alone can materially reduce your cost per claim before

any other intervention kicks in. For guidance on how early reporting cuts costs and improves outcomes, see this primer on

early reporting best practices.

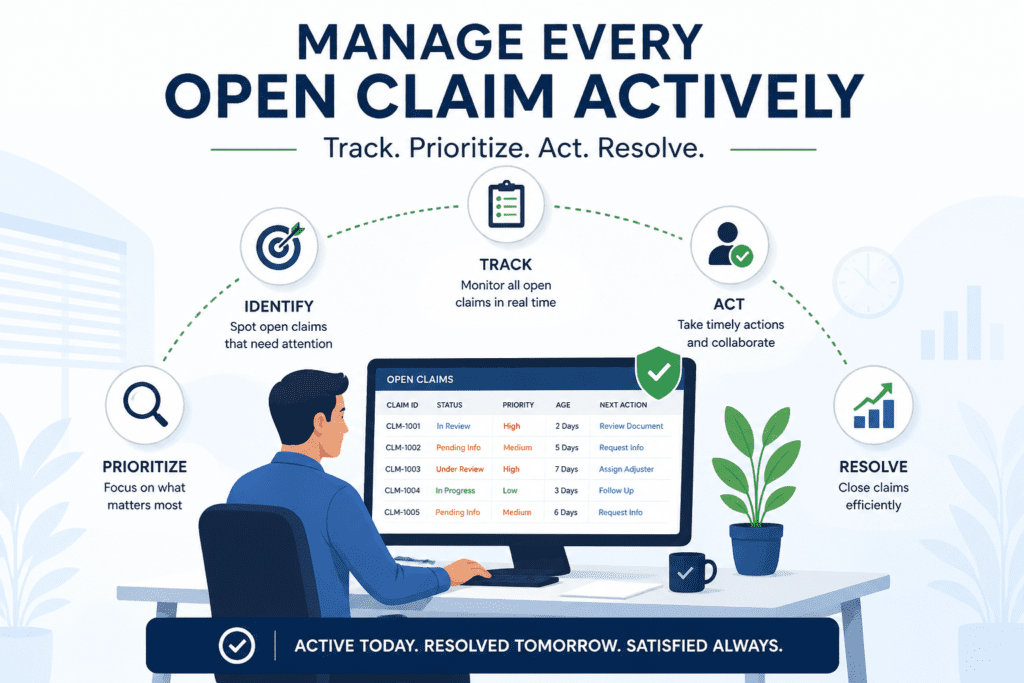

5. Manage every open claim actively

Reporting fast gets you in the game. Active claims management keeps costs from compounding after the initial report. That

means directing injured employees to employer-approved clinics rather than emergency rooms where possible, establishing

early nurse triage, and maintaining regular contact with the injured employee throughout recovery.

One employer’s 18-month proactive management effort produced a 35% reduction in annual incurred losses, totaling

approximately $495,000 in savings. That included a 21% decrease in average claim duration and a drop in litigated claims

from 14% to 9%. The protocol isn’t complicated: assign a dedicated contact, keep documented touchpoints with the

employee, and review open reserve amounts regularly with your adjuster.

KPIs to track: average days to report, litigated claim percentage, cost per claim.

6. Launch a return-to-work program to reduce workers' compensation costs

Return-to-work programs consistently produce the strongest documented savings of any single tactic on this list; a wellstructured RTW program is discussed in detail by industry experts (return-to-work best practices). A 10-year study showed

lost-time claims decreased 73% and total workers’ comp costs fell 54% after a formal program launched. A modified-duty

return-to-work approach reduced claim costs by close to 80% in a separate documented case study. Roto-Rooter Services

cut annual workers’ comp costs, which had ranged from $1.4 million to $1.85 million, down to $365,000 after launching

their program.

The mechanics are straightforward. A return-to-work program assigns modified or transitional duties to injured employees

as soon as they are medically cleared for light duty, rather than leaving them on full indemnity during recovery. Transitional

work can be on-site with modified tasks or off-site through community partnerships. The essentials are a written RTW

policy, detailed job demand analyses for each role, a designated HR point of contact, and a documented communication

protocol with treating physicians.

ROI for well-designed programs runs $8 to $15 returned for every $1 invested. KPIs to track: return-to-work rate within 30 days, average claim duration, indemnity days per claim.

ROI for well-designed programs runs $8 to $15 returned for every $1 invested. KPIs to track: return-to-work rate within 30 days, average claim duration, indemnity days per claim.

7. Screen high-risk hires before the first day of work

Hiring decisions are an underused cost lever for workers’ comp. A cross-sectional study of approximately five million

individuals found that employees who received post-offer employment testing had significantly lower workers’ comp costs

in year one, averaging $68 lower per employee in workers’ comp costs and $797 in total first-year savings per employee.

Scaled to 1,000 hires, that’s close to $800,000 in first-year savings from a screening protocol alone.

The highest impact is in physically demanding roles: lifting, carrying, climbing, and repetitive motion tasks. Pre-employment

physicals identify mismatches between job demands and a candidate’s physical capacity before an injury-prone placement

happens. Screenings must be post-offer, job-related, and consistent with ADA and EEOC business necessity standards. Drug

testing for safety-sensitive roles complements the physical screening layer. For practical employer benefits of preemployment physicals, see dedicated employer resources on occupational medicine and pre-employment screening.

KPI to track: first-year claim rate for screened versus unscreened hire cohorts.

KPI to track: first-year claim rate for screened versus unscreened hire cohorts.

8. Reduce workers' compensation costs by restructuring your rated payroll

Workers’ comp premiums are calculated on payroll. When a supplemental health benefits layer is added through a properly

structured program, such as a Section 125 arrangement, a portion of employee compensation shifts into a pre-tax benefit.

That reduces the taxable and workers’ comp-rated payroll base. Less rated payroll means a lower premium calculation that

scales directly with workforce size.

This is a legal, IRS-compliant strategy under Section 125 of the Internal Revenue Code that works alongside existing payroll

systems and current group health insurance. Nothing is replaced or disrupted. Depending on state, classification codes, and

payroll size, the reduction in workers’ comp-rated payroll can drive meaningful estimated workers’ comp savings, with

some employers in high-cost states like California, Texas, and Florida seeing the largest impact, where base rates and

classification codes carry elevated multipliers. The 35% savings figure represents an upper-bound vendor estimate; actual

results vary by workforce composition and state.

Employer Benefits Plan conducts a structured eligibility review covering workforce size, W-2 employee structure, and

payroll composition to estimate what this strategy may produce for a specific business. The review also quantifies

estimated FICA payroll tax savings, approximately $640 per participating W-2 employee based on the program’s

methodology, making the total savings picture considerably larger than workers’ comp alone. That figure reflects the

employer-side FICA impact of shifting compensation into pre-tax benefits and will vary by employee compensation level.

The initial consultation is free and produces a personalized savings estimate before any commitment is required. For more

information, visit Employer Benefits Plan.

Put these workers' comp cost reduction strategies to work in the right order

Start with the classification audit because misclassified codes inflate your base premium regardless of how well everything

else runs. From there, build your safety program to move EMR over the next 12 to 24 months while locking in the 24-hour

reporting protocol immediately. Add a return-to-work policy and pre-employment screening for high-risk roles as the next

layer, then explore the supplemental benefits structure once the operational fundamentals are in place.

These strategies compound. An employer who corrects class codes, drops EMR from 1.2 to 0.9, and adds a supplemental

benefits layer is looking at a materially different premium within 18 to 24 months. Each tactic reinforces the others: fewer

claims improve EMR, lower rated payroll reduces the base the EMR multiplies against, and better hires produce fewer

claims to begin with.

If you want to see what the supplemental benefits strategy specifically would produce for your payroll and classification

codes, start with a savings review through Employer Benefits Plan. The estimate is personalized, the consultation is free,

and the numbers are specific to your workforce. Workers’ comp costs come down when the right levers are identified and

pulled in sequence, not by chance. Knowing which levers exist is where the process starts; using them consistently is where

the savings accumulate.

Disclaimer

This article is for general business education only and is not legal, tax, insurance, or workers’ compensation advice. Savings

estimates vary based on employer-specific facts, payroll structure, classification codes, carrier rules, state requirements, employee

participation, and implementation details. Employers should consult appropriate licensed, legal, tax, insurance, or compliance

professionals before making plan or insurance decisions.

Review Whether This Strategy May Fit Your Workforce

Employer Benefits Plan helps employers review whether a supplemental benefits and payroll-savings strategy may support potential savings and employee benefit value.